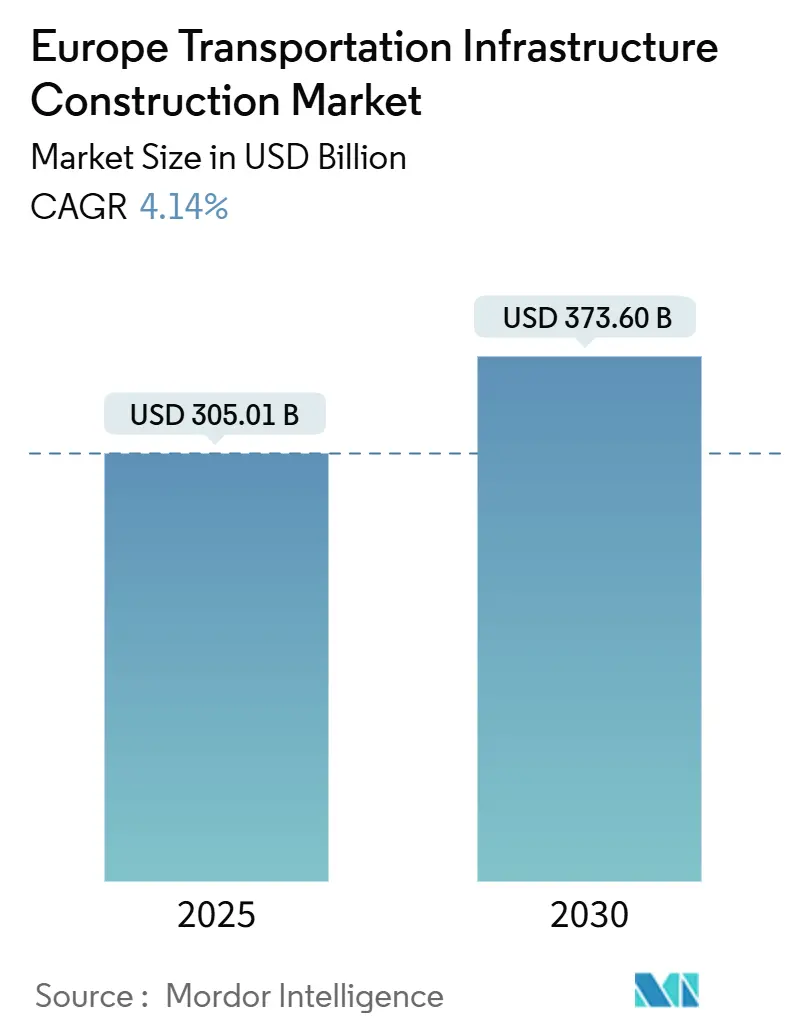

Market Overview

Study Period 2019 - 2030 Base Year For Estimation 2024 Forecast Data Period 2025 - 2030 Market Size (2025) USD 305.01 Billion Market Size (2030) USD 373.60 Billion Growth Rate (2025 - 2030) 4.14% CAGR Market Concentration Medium Major Players

*Disclaimer: Major Players sorted in no particular order

Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0.

Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0.

Europe Transportation Infrastructure Construction Market Analysis by Mordor Intelligence

Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0.

Europe Transportation Infrastructure Construction Market Analysis by Mordor Intelligence

The Europe Transportation Infrastructure Construction Market size stands at USD 305.0 billion in 2025 and is forecast to reach USD 373.6 billion by 2030, reflecting a 4.14% CAGR over the period. The growth path is steered by record EU funding, notably a USD 7.7 billion tranche from the Connecting Europe Facility 2.0 in 2024 that prioritized climate-smart, cross-border links. Rapid policy alignment on completing the Trans-European Transport Network (TEN-T) core by 2030, coupled with military-mobility upgrades, has created a predictable, long-term project queue. Rail electrification, hydrogen corridors, and AI-enabled maintenance now vie for the same budget that once fored highway widening, tilting capital toward lower-carbon assets. Contractors with digital design capabilities and ESG-compliant supply chains are winning bids as funding rules explicitly score sustainability metrics. At the same time, widespread labor shortages and extreme-weather repair bills temper the overall expansion pace, nudging private partners to absorb risk through concession agreements.

Key Report Takeaways

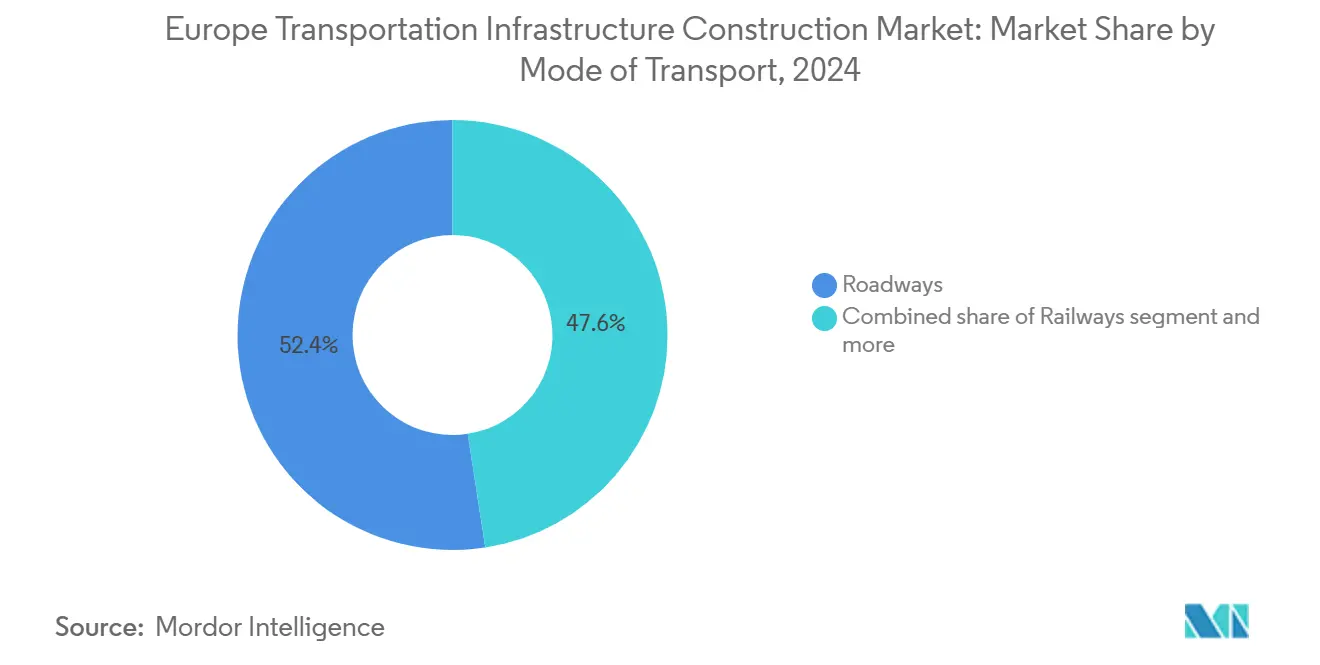

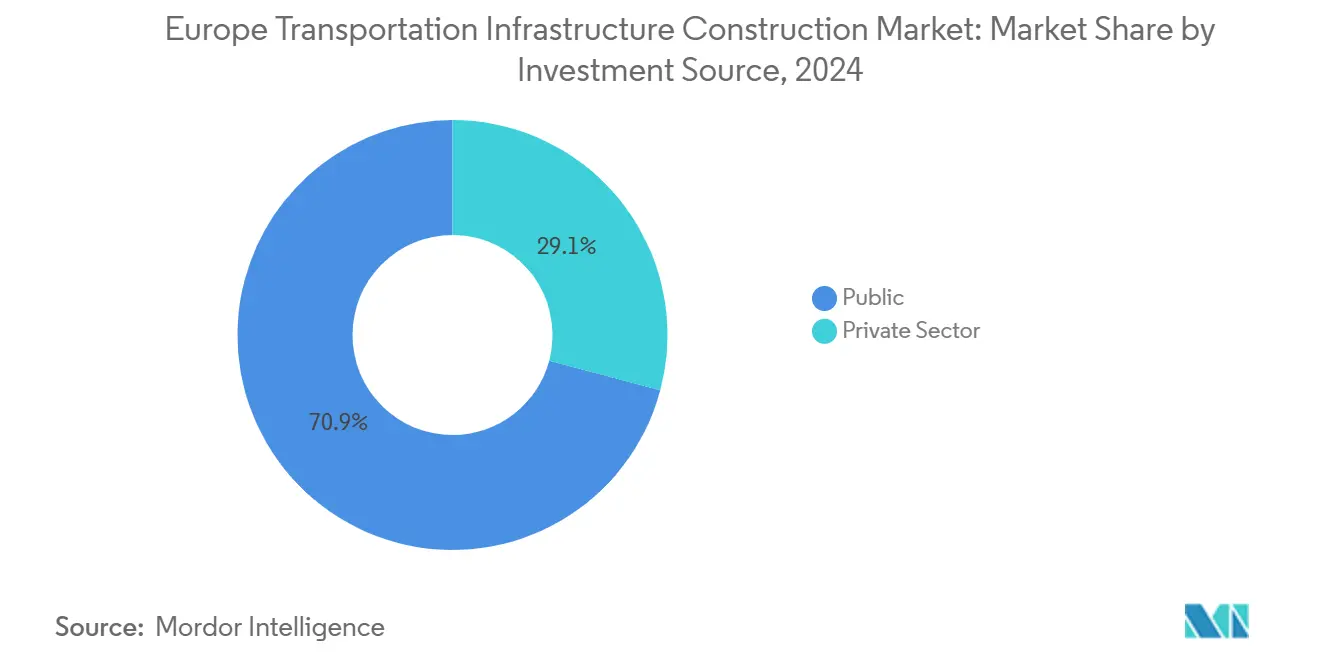

By mode of transport, roadways held 52.43% of the Europe transportation infrastructure construction market share in 2024. Railways are projected to post the fastest 5.18% CAGR through 2030 within the Europe transportation infrastructure construction market. By construction activity, new builds dominated 73.54% of the Europe transportation infrastructure construction market size in 2024, and are growing at a 4.93% CAGR. By investment source, public funding commanded 70.86% of the Europe transportation infrastructure construction market size in 2024, while private capital is the fastest-growing source with a 5.51% CAGR. By geography, Germany led with 17.54% revenue share in 2024, whereas Spain is set to record the highest 5.73% CAGR during 2025-2030 in the Europe transportation infrastructure construction market. Europe Transportation Infrastructure Construction Market Trends and InsightsDrivers Impact Analysis

Driver (≈) % Impact on CAGR Forecast Geographic Relevance Impact Timeline Sustainable, energy-efficient infrastructure +1.2% Germany, France, Netherlands Medium term (2-4 years) Surge in new road & rail capacity +0.9% Germany, Spain, Poland, Eastern Europe Short term (≤ 2 years) EU funding programs (CEF 2.0, RRF) +0.8% EU-wide, cohesion countries emphasized Short term (≤ 2 years) Climate-resilient retrofitting mandates +0.7% Alpine, coastal, Northern Europe zones Medium term (2-4 years) Military-mobility corridor upgrades +0.4% Eastern Europe, Baltic States, Germany Short term (≤ 2 years) AI-enabled predictive maintenance +0.3% Germany, Netherlands, France Long term (≥ 4 years) Source: Mordor Intelligence

Development of Sustainable, Energy-Efficient Transport Infrastructure

The European Commission earmarked USD 464.2 million for 39 alternative-fuel projects in 2025, accelerating deployment of 4,900 charging points across the TEN-T. Hydrogen corridors such as H2Med (USD 2.8 billion) demand tunnels, stations, and pipelines engineered for dual energy-mobility use. New regulations fix binding national targets, so builders now integrate battery storage, on-site renewables, and smart-grid links by default. Digital project models, as trialed on VINCI’s A7 motorway in Germany, shrink maintenance costs through predictive analytics. These shifts embed sustainability into core design, locking in multi-year demand for specialized civil contractors[1]Ileana Ionescu, “Alternative Fuels Infrastructure Facility—2025 Award Decision,” European Climate, Infrastructure and Environment Executive Agency, cinea.europa.eu.

Surge in Demand for New Road & Rail Capacity

Mega-schemes such as the Grand Paris Express, 200 km of track, 68 stations, and a USD 62.1 billion budget, illustrate the region’s appetite for fresh capacity. Spain follows suit: USD 265.1 million in EU grants cover 22 projects spanning seven regions, with USD 85.8 million devoted to Zaragoza-Teruel-Sagunto rail electrification. Cross-border lines draw equal focus; Rail Baltica’s 870 km rail will slash Tallinn-Warsaw trel to seven hours, anchoring modal shift from air to rail. Order books reflect the boom: Bouygues and Eiffage each logged 40%-plus backlog growth in 2024. Governments such as the Netherlands he already ring-fenced USD 16.2 billion for 2025 transport works, ensuring near-term project starts.

EU Funding Programs (CEF 2.0, RRF) Unlocking Project Pipeline

CEF 2.0 sets aside USD 28.4 billion for 2021-2027, with USD 12.4 billion funneled to cohesion states and another USD 1.9 billion to dual-use military routes. The structure rewards projects ticking sustainability and cross-border boxes, pushing firms toward consortium bids capable of handling procurement complexity. The Recovery and Resilience Facility adds long-tenor loans, highlighted by the USD 330 million EIB tranche for Romania’s Cluj-Napoca rail electrification. Subsidy rates hitting 85% on Rail Baltica temporarily distort competition in for of large multinationals that can nigate EU compliance. Contractors, therefore, invest in grant-writing teams and ESG reporting to secure a share of the ballooning pipeline.

Climate-Resilient Retrofitting Mandates Under 2024 TEN-T Revision

From July 2024, every TEN-T asset must meet minimum resilience standards, turning adaptation into a standalone revenue stream. Austria’s 25-day rail shutdown for drainage upgrades and Network Rail’s USD 3.1 billion climate plan typify the new retrofit agenda. Projects now specify reinforced embankments, heat-tolerant track, and nature-based flood buffers, escalating bill-of-materials costs. Specialized design consultancies gain traction, while insurers demand stricter risk quantification, reshaping contract models. Over time, resilience spending cushions any slowdown in new-build activity, keeping the Europe transportation infrastructure construction market on a steady growth slope[2]Pål E. Dahlberg, “Revised TEN-T Regulation 2024/1801,” Official Journal of the European Union, eur-lex.europa.eu.

Restraints Impact Analysis

Restraint (≈) % Impact on CAGR Forecast Geographic Relevance Impact Timeline Public-funding gaps & fiscal rules -0.8% Germany, France, Italy Medium term (2-4 years) Rising climate-related repair costs & delays -0.6% Alpine, coastal, extreme-weather zones Short term (≤ 2 years) Shortage of specialized tunneling/electrification talent -0.5% Germany, Netherlands, Austria Medium term (2-4 years) Environmental litigation under biodiversity rules -0.3% EU-wide, cross-border projects Long term (≥ 4 years) Source: Mordor IntelligencePersistent Public-Funding Gaps & Fiscal Rules

Germany invests only 2.1% of GDP in public infrastructure versus the 3.7% EU mean, leing a USD 495.0 billion shortfall by 2030. Debt-brake rules cap borrowing, nudging governments toward costly PPP deals that add up-front transaction fees and longer negotiation cycles. Deutsche Bahn alone needs USD 165 billion through 2034, yet faces political resistance to deficit spending. One-third of EU municipalities report under-investment in transport, highlighting a structural demand-supply gap. While private bonds ease some pressure, weaker regions struggle to attract investors, dampening the Europe transportation infrastructure construction market’s full potential[3]Thomas Henrichs, “Deutsche Bahn Investment Gap Report 2025,” Deutsche Bahn AG, deutschebahn.com.

Rising Climate-Related Repair Costs & Delays

Extreme weather is diverting capital from expansion to emergency fixes. Switzerland’s Gotthard Base Tunnel required USD 165 million in post-derailment repairs and stayed closed for 389 days. The Paris-Milan rail link cost USD 14.3 million to restore after landslides, delaying corridor capacity for 19 months. Heat-we damage on German autobahns prompts overnight concrete replacements, straining labor rosters. EU researchers warn that cumulative climate damage could top USD 971 billion by 2100 under worst-case scenarios. Contractors now budget for rapid-response teams, but recurrent shocks still siphon resources away from new projects.

Segment AnalysisBy Mode of Transport: Railways Spur Modal Shift

Railways account for the fastest 5.18% CAGR, although roadways remain atop the Europe transportation infrastructure construction market with a 52.43% revenue slice in 2024. The Brenner Base Tunnel, stretching 64 km under the Alps to move 50 million tons of annual freight, headlines the rail surge. The Lyon-Turin link adds another 57.5 km of high-speed tunnel, with USD 4.4 billion in civil contracts already signed. Such mega-projects make the Europe transportation infrastructure construction market size for rail the standout growth vector.

Roadway investment still rolls on, epitomized by the A24 Blankenburgverbinding that opened in December 2024 with smart tolling and twin tunnels. Yet regulatory pressure trims future highway share by steering freight to waterways like the USD 7.7 billion Seine-Nord Europe Canal. Digital layers, ERTMS Level 2 on 270 km of Dutch track, further tilt capital toward rails as specification complexity rises.

Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0.

Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0.

Note: Segment shares of all individual segments ailable upon report purchase

By Construction Activity: New Builds Dominate

New projects captured 73.54% of the Europe transportation infrastructure construction market share in 2024 and are forecast to grow 4.93% annually through 2030. Network-completion deadlines spur greenfield lines such as Rail Baltica, whose budget swelled to USD 26.4 billion for 870 km of double-track. Likewise, the Fehmarnbelt immersed tunnel involves 79 precast elements weighing 73,000 tons each, demanding industrial-scale fabrication yards.

Renovations focus on climate retrofits and digital upgrades. Austria’s Koralm Railway fuses 130 km of new track with modernizing legacy segments to hit 250 km/h. Urban retrofits like Grand Paris Express must tunnel beneath live metro lines, triggering archaeological surveys and strict vibration limits that stretch timelines. While smaller in volume, retrofit margins improve as clients pay premiums for minimal service disruption.

By Investment Source: Private Capital Accelerates

Public money still controls 70.86% of 2024 spend, but private finance posts a 5.51% CAGR, making it the fastest-rising wallet in the Europe transportation infrastructure construction market. Germany’s USD 550 billion modernization fund aims for 90% private participation, a watershed for concession models. EU-backed project bonds trim sovereign borrowing and spread risk, exemplified by the Fehmarnbelt blend of user tolls with USD 1.4 billion in EU grants.

Tech-hey assets attract private equity chasing steady cash flows from digital services. VINCI embeds AI-based asset management into concession bids, capturing long-term fee streams beyond construction phases. The Corporate Sustainability Reporting Directive further lures ESG-focused funds, aligning investor mandates with green-infrastructure pipelines.

Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0.

Geography Analysis

Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0.

Geography Analysis

Germany generated 17.54% of 2024 revenue, cementing its lead in the Europe transportation infrastructure construction market. Flagship schemes like Stuttgart 21, whose bill ballooned from USD 3.3 billion to USD 12.1 billion, reveal both ambition and complexity. Deutsche Bahn still requires USD 165 billion by 2034 for network renewal, guaranteeing a thick backlog. Chronic underspend relative to GDP means pent-up demand will support a steady order flow despite fiscal caps.

Spain is the acceleration story, tracking a 5.73% CAGR through 2030. Securing USD 265.1 million in EU grants during 2024 alone, the country electrifies inland routes and ports while anchoring the USD 2.8 billion H2Med hydrogen corridor. EU regulations that push renewable integration dovetail with Spain’s solar leadership, amplifying project momentum.

France, the United Kingdom, and the Netherlands rank as mature but opportunity-rich. France’s USD 62.1 billion Grand Paris Express and delayed CDG Express underscore the scale of urban retrofits. The Netherlands budgets USD 16.2 billion for 2025 improvements, from highway tunneling to ERTMS rollout. The UK moves ahead with the GBP 10 billion (USD 11.0 billion) Lower Thames Crossing slated for late-2025 ground-breaking. Cohesion-fund recipients in Eastern Europe enjoy higher EU subsidy ratios, lifting project viability even in smaller economies.

Competitive Landscape

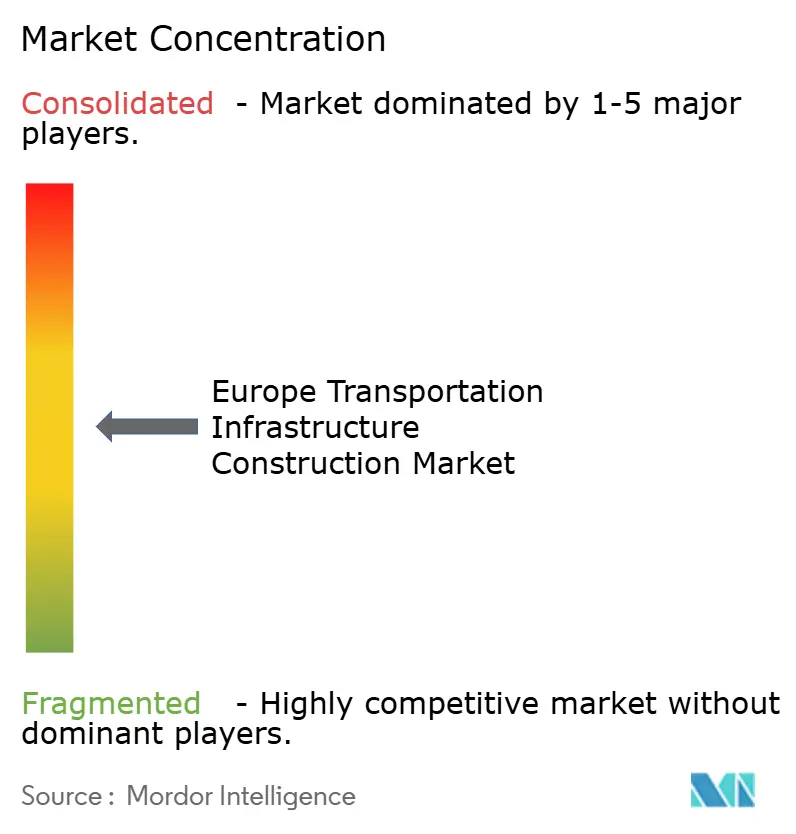

The market remains moderately fragmented but is tilting toward consolidation. Multinationals such as VINCI posted record USD 78.8 billion revenue in 2024, buoyed by airport acquisitions that diversify income streams. ACS-Hochtief reshaped its portfolio by merging U.S. subsidiaries and picking up Irish MEP specialist Dornan for USD 1.2 billion, expanding turnkey capability across regions. Webuild secured USD 8.3 billion of new orders and now holds a USD 71.5 billion backlog, spotlighting a pivot toward rail mega-projects.

Technology investment differentiates leaders. BIM, digital twins, and AI maintenance platforms open new revenue lines in operations and cut warranty costs, allowing aggressive concession bids. ESG mandates add another filter; Ferrovial targets carbon neutrality by 2050, aligning with lender criteria. Mid-sized regional firms survive by specializing, tunneling in Austria, electrification in the Netherlands, or coastal defenses in Denmark, yet often partner with giants for cross-border bids.

White-space niches include climate-adaptation retrofits, hydrogen-ready tunnels, and dual-use military corridors. These areas blend civil works with new engineering disciplines, raising barriers to entry and giving incumbents a first-mover edge. EU procurement rules that for proven past performance further reinforce the incumbency advantage, suggesting a gradual rather than a rapid market shake-out.

Europe Transportation Infrastructure Construction Industry LeadersVINCI SA

ACS Group (incl. HOCHTIEF)

Bouygues Construction

Eiffage SA

Skanska AB

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0.

Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0.

Recent Industry Developments

February 2025: European Commission committed USD 464.2 million to 39 alternative-fuel infrastructure projects, adding 4,900 charging points across TEN-T.October 2024: European Investment Bank supplied USD 330 million for Romania’s Cluj-Napoca–Episcopia Bihor rail electrification, part of a USD 2.2 billion package.August 2024: Gannett Fleming acquired TranSystems for USD 1.3 billion, forming a 5,000-employee design powerhouse.December 2024: The Netherlands opened the A24 Blankenburgverbinding highway, featuring twin immersion tunnels and smart tolls.

Table of Contents for Europe Transportation Infrastructure Construction Industry Report

Recent Industry Developments

February 2025: European Commission committed USD 464.2 million to 39 alternative-fuel infrastructure projects, adding 4,900 charging points across TEN-T.October 2024: European Investment Bank supplied USD 330 million for Romania’s Cluj-Napoca–Episcopia Bihor rail electrification, part of a USD 2.2 billion package.August 2024: Gannett Fleming acquired TranSystems for USD 1.3 billion, forming a 5,000-employee design powerhouse.December 2024: The Netherlands opened the A24 Blankenburgverbinding highway, featuring twin immersion tunnels and smart tolls.

Table of Contents for Europe Transportation Infrastructure Construction Industry Report

1. Introduction

1.1 Study Assumptions & Market Definition 1.2 Scope of the Study2. Research Methodology

3. Executive Summary

4. Market Landscape

4.1 Market Overview 4.2 Market Drivers 4.2.1 Development of sustainable, energy-efficient transport infrastructure 4.2.2 Surge in demand for new road & rail capacity 4.2.3 EU funding programmes (CEF 2.0, RRF) unlocking project pipeline 4.2.4 Climate-resilient retrofitting mandates under 2024 TEN-T revision 4.2.5 Military-mobility corridor upgrades post-Ukraine war 4.2.6 AI-enabled predictive maintenance lowering lifecycle costs 4.3 Market Restraints 4.3.1 Persistent public-funding gaps & fiscal rules 4.3.2 Rising climate-related repair costs & delays 4.3.3 Shortage of specialised tunnelling / electrification talent 4.3.4 Environmental litigation under new biodiversity rules 4.4 Value / Supply-Chain Analysis 4.4.1 Overview 4.4.2 Real Estate Developers and Contractors - Key Quantitative and Qualitative Insights 4.4.3 Architectural and Engineering Companies - Key Quantitative and Qualitative Insights 4.4.4 Building Material and Equipment Companies - Key Quantitative and Qualitative Insights 4.5 Government Initiatives & Vision 4.6 Regulatory Outlook 4.7 Technological Outlook 4.8 Industry Attractiveness - Porter's Five Force Analysis 4.8.1 Threat of New Entrants 4.8.2 Bargaining Power of Suppliers 4.8.3 Bargaining Power of Buyers 4.8.4 Threat of Substitutes 4.8.5 Intensity of Competitive Rivalry 4.9 Pricing (Construction Materials) and Construction Cost (Materials, Labour, Equipment) Analysis 4.10 Comparison of Key Industry Metrics of Top European Countries 4.11 Key Upcoming/Ongoing Projects (with a focus on Mega Projects)5. Market Size & Growth Forecasts (Value, In USD Billion)

5.1 By Type 5.1.1 Roadways 5.1.2 Railways 5.1.3 Airways 5.1.4 Ports and Inland Waterways 5.2 By Construction Type 5.2.1 New Construction 5.2.2 Renovation 5.3 By Investment Source 5.3.1 Public 5.3.2 Private 5.4 By Geography 5.4.1 Germany 5.4.2 United Kingdom 5.4.3 France 5.4.4 Spain 5.4.5 Netherlands 5.4.6 Rest of Europe6. Competitive Landscape

6.1 Market Concentration 6.2 Strategic Moves 6.3 Market Share Analysis 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as ailable, Strategic Information, Products & Services, Recent Developments) 6.4.1 VINCI SA 6.4.2 ACS Group (incl. HOCHTIEF) 6.4.3 Bouygues Construction 6.4.4 Eiffage SA 6.4.5 Skanska AB 6.4.6 Ferrovial SE 6.4.7 Webuild SpA 6.4.8 Colas SA 6.4.9 Balfour Beatty plc 6.4.10 BAM Group 6.4.11 Kier Group 6.4.12 Costain Group 6.4.13 Implenia AG 6.4.14 PORR AG 6.4.15 Salcef Group 6.4.16 NCC AB7. Market Opportunities & Future Outlook

7.1 White-space & Unmet-Need Assessment

Europe Transportation Infrastructure Construction Market Report Scope

Europe Transportation Infrastructure Construction Market Report Scope

Transportation infrastructure is referred to as the framework that facilitates the transportation system. Roads, railways, ports, and airports are all part of it. Daily, transportation infrastructure connects people to jobs, health care, education, etc. It makes it easier to provide and receive goods and services worldwide.

The European transportation infrastructure construction market is segmented by mode (roads, railways, airways, and waterways) and country (Germany, United Kingdom, France, Spain, Italy, the Netherlands, and the Rest of Europe). The report offers market size and forecast values (in USD) for all the above segments.

By Type Roadways Railways Airways Ports and Inland Waterways By Construction Type New Construction Renovation By Investment Source Public Private By Geography Germany United Kingdom France Spain Netherlands Rest of Europe By Type Roadways Railways Airways Ports and Inland Waterways By Construction Type New Construction Renovation By Investment Source Public Private By Geography Germany United Kingdom France Spain Netherlands Rest of Europe

Key Questions Answered in the Report

How large is the Europe transportation infrastructure construction market in 2025?

Key Questions Answered in the Report

How large is the Europe transportation infrastructure construction market in 2025?

It is valued at USD 305.0 billion, with a projected rise to USD 373.6 billion by 2030 at a 4.14% CAGR.

Which transport mode is growing fastest in Europe through 2030?Railways lead with a 5.18% CAGR, propelled by high-speed and electrification mega-projects.

Why is private investment increasing in European transport projects?Fiscal caps on public borrowing and EU project-bond schemes are steering more projects toward PPP and concession models that rely on private capital.

What is the main constraint on project delivery today?Severe shortages of skilled tunneling and electrification workers are delaying schedules and raising costs.

Page last updated on: August 22, 2025

Automated Barriers And Bollards Market Industry Trends in Eastern Europe Construction Europe Building And Construction Sheets Market Europe Manufactured Homes Industry Europe Prefabricated Buildings Market Size Infrastructure Market